Social and pension security for entrepreneurs

YEL insurance contributions and your future employment pension are based on your reported YEL income, which the pension provider confirms for your YEL insurance. In addition to your pension, the YEL income also has an impact on the level of the different benefits and pensions you may receive. For this reason, it is essential that your YEL income be dimensioned accurately in order to provide you with the proper security throughout your working career.

You can see your own pension record in Elo's Online Service for private customers.

Your YEL income affects the following pensions and benefits:

Illness of entrepreneur

Starting from 1 January 2020 the annual income serves as the basis for the amount of the sickness allowance provided by Kela. The annual income is calculated from the reference period of 12 calendar months prior to the calendar month that precedes the initiation of your work disability. For self-employed persons, the basis for the calculation of the annual income is the YEL income. If the amount of the YEL income has changed during the 12-month period in question, the average income will be used.

YEL insurance cannot be interrupted due to a brief period of illness. It can, however, be terminated due to an extended sick leave. In this case, you will need to take a new YEL insurance policy when you return to work after your sick leave.

Entrepreneur's parental leave

The annual income serves as the basis for the amount of the maternity, special maternity, paternity, parental and partial parental allowance provided by Kela. The annual income is calculated from the reference period of 12 calendar months prior to the calendar month that precedes the initiation of your work disability. For self-employed persons, the basis for the calculation of the annual income is the YEL income. If the amount of the YEL income has changed during the 12-month period in question, the average income will be used.

If you are not working during your family leave, your YEL insurance can be terminated as ending on your last day of work. In this case, you will need to take a new insurance policy when you return to work. If you are working during your family leave, your YEL insurance is not terminated. It may, however, be necessary to adjust your YEL income if your work input in the company is reduced during the family leave.

Entrepreneur's unemployment

A self-employed person may have the possibility to receive Kela’s basic unemployment allowance or, as a member of an unemployment fund, an earnings-related unemployment allowance if that person’s YEL income has been at least the minimum required for unemployment security, which in 2025 is 15,128 €.

One requirement to receive an unemployment allowance is that your entrepreneurial activities must be considered substantial in the manner intended by the Unemployment Security Act. If your YEL income falls below the minimum you can still apply for a labour market subsidy from Kela. If you are a member of an unemployment fund, the amount of your earnings-related unemployment allowance is based on your YEL income.

Further information:

Entrepreneur's accident insurance

The annual earnings used for voluntary accident insurance policies intended for self-employed persons are bound to their confirmed YEL income. Your YEL income also affects any compensation for loss of earnings and pensions resulting from an occupational accident. In order to be entitled to accident insurance for a self-employed person, you must have a valid YEL insurance policy.

Further information:

Pensions and rehabilitation

Employment pension insurance provides you with security when your income changes due to old age, disability or the death of a family provider. A self-employed person’s pension accrues in accordance with the confirmed YEL income reported for the YEL insurance policy. YEL income not only affects the amount of your future old-age pension but also serves as the foundation for other pensions and benefits under employment pension legislation, which you may be entitled to already prior to reaching the pensionable age for old-age pension.

Pension accrues for all ages at an annual rate of 1.5 per cent of the YEL income. However, during the transition period of 2017–2025, pension will accrue at a rate of 1.7 per cent of the YEL income for those aged 53–62. Read more about

Income limits 2025

- Minimum 9,208.43 €/year

- Maximum 209,125.00 €/year

- Minimum for unemployment security 15,128.00 €/year

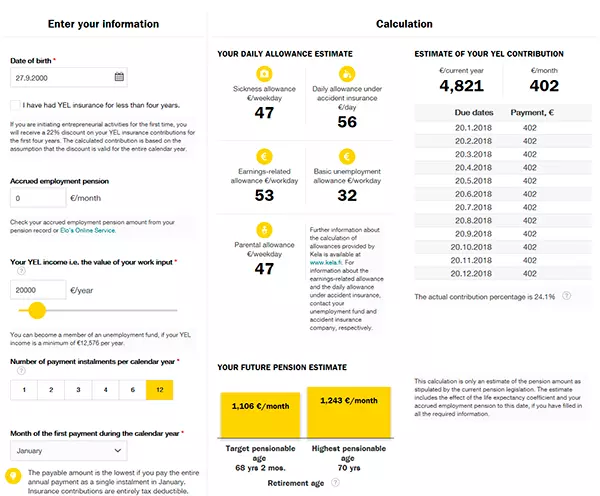

The YEL calculator shows you what type of security your current income would provide for various situations. You can see how changes in your income would affect your pension and social security and the impact such changes would have on your insurance contributions.