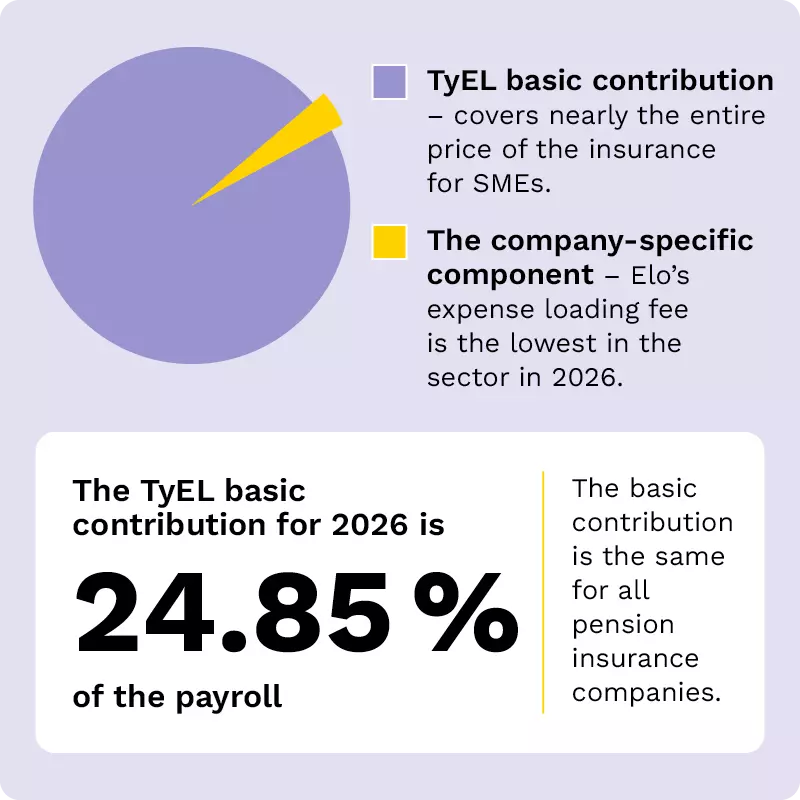

Because the TyEL basic contribution, which covers the biggest share of the price of TyEL insurance, is the same in all pension insurance companies, it is worth focusing on the total benefit when comparing insurance:

- Smooth digital tools and personal customer service save time.

- Work ability management services that support your company in a suitable way improve the wellbeing of your employees and lower disability costs.

- The company-specific expense loading fee, constancy and scale discounts, and client bonuses can bring savings.

Comparing TyEL insurance policies is more challenging than, for example, competing a company’s non-life insurance policies, because each company’s situation and therefore the amount of the TyEL contribution is individual.

The customer-specific part of the TyEL contribution is affected by, among other things, the length of the customer relationship in the current company, the amount of wages paid, and the discounts and client bonuses offered by the pension insurance company. For small and medium sized enterprises, the effect of the company-specific part on the price of TyEL insurance is usually small.

When comparing pension insurance companies, keep in mind at least the following points:

- What kind of companies and what size of companies does the pension insurance company focus on?

- Does your company get personal support and a named contact person?

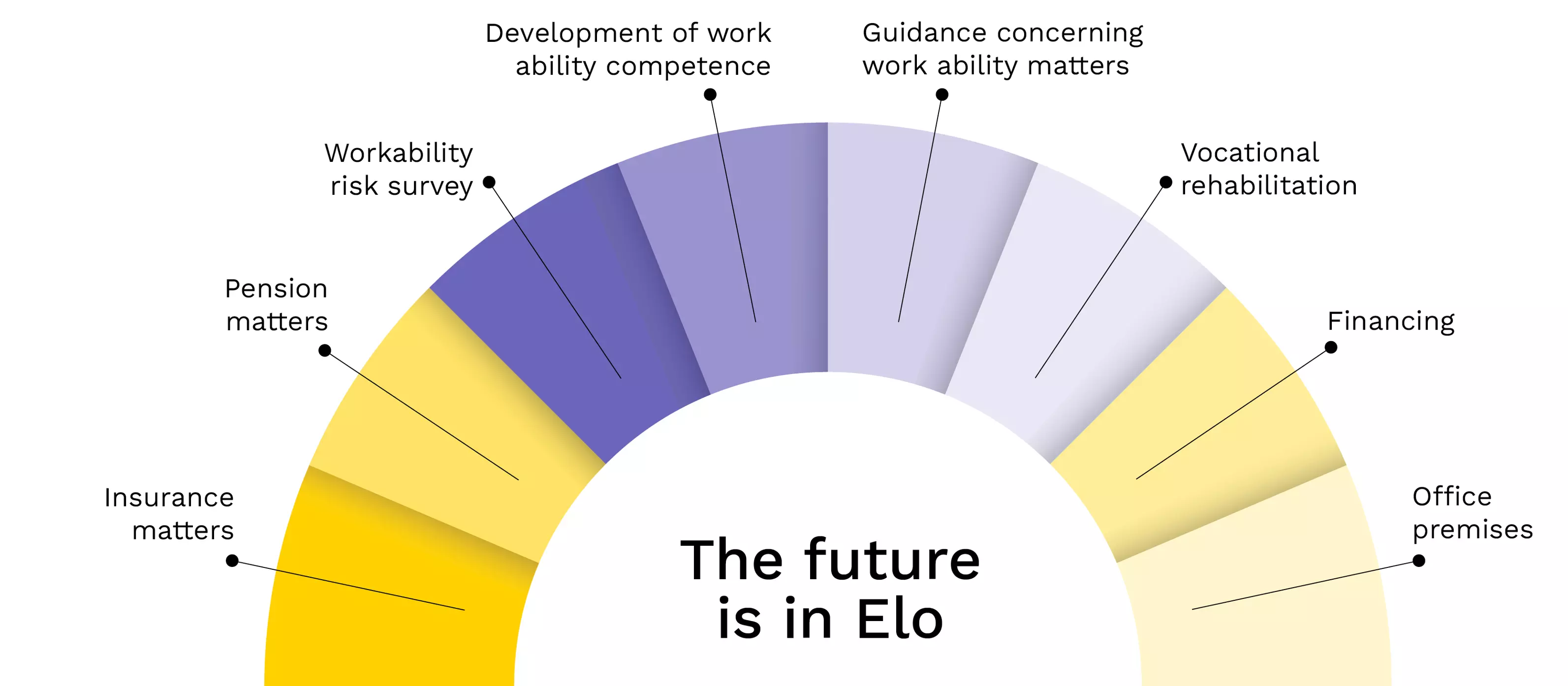

- What kind of value-added services, such as work ability management services, vocational rehabilitation or financing, does the pension insurance company offer?

- Is the online service easy to use?

- What kind of scale or constancy discounts and client bonuses does the pension insurance company offer?

Read more about how the price of TyEL insurance is formed